Byron Wien, who passed away in 2023, was one of Wall Street’s most respected strategists. Best known for his long career at Morgan Stanley, he gained prominence for his annual “10 Surprises” list — forecasts he believed had more than a 50% chance of occurring, even though markets assigned them odds below one-third.

A few institutions have attempted to carry on his tradition, and U.K.-based Variant Perception has now taken up the mantle for a second year. The firm continues to follow Wien’s original framework of “more likely than the market thinks.”

Their broad outlook for next year? A generally healthy economic environment. Variant Perception expects U.S. nominal GDP growth to exceed 5%, combining economic expansion and inflation. Historically, this type of backdrop has supported equities, placed a floor under bond yields, and strengthened the U.S. dollar — dynamics that have already begun to play out over the past two months.

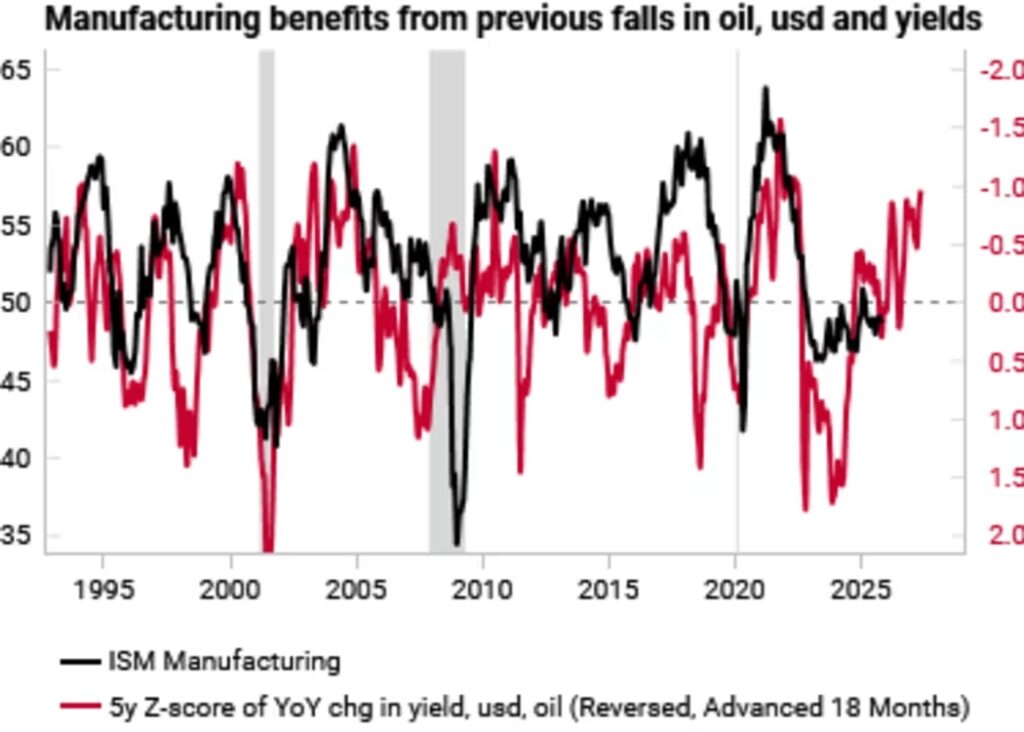

Even so, they note this is typically the period when earlier declines in key variables — such as yields or the dollar — start to spur manufacturing activity. While the macro setup looks constructive, they warn that stretched valuations and thin risk premiums in credit and equities remain a challenge.

This, they say, argues for rotating toward emerging markets, value stocks, and other laggards. In short: “a valuation problem, not a macro problem.”

Here are Variant Perception’s 10 “surprises” for the year ahead:

- Trump’s capex boom arrives a year late and expands beyond AI

- U.S. economic growth beats expectations despite a subdued labor market

- Housing disinflation undermines the narrative of sticky inflation

- U.S. 10-year yields hover near 4% and remain range-bound

- Value stocks outperform growth stocks

- G10 FX divergence: APAC currencies (AUD & NZD) outperform Europe (EUR & GBP)

- Emerging-market equities outperform developed markets, led by Brazil

- Oil trades below $50 and above $75 at different points in the year

- China tech stocks outperform U.S. tech stocks

- Capital cycle winners: U.S. regional banks and energy services outperform

The first surprise — a broader capex boom — merits deeper attention. With tariff policy now largely clarified, bank lending surveys suggest that financial institutions are easing standards and seeing stronger commercial loan demand. Corporations may also benefit from recent tax changes allowing 100% bonus depreciation and immediate expensing of R&D costs.

Meanwhile, declines in oil prices, the U.S. dollar, and yields often provide a tailwind for manufacturing, aligning with past cyclical patterns.

However, this manufacturing rebound may not translate into stronger job growth. Variant Perception sees similarities to the 2002–2003 “jobless recovery,” when productivity gains and accommodative monetary policy supported output without significantly boosting employment.

Their view on oil also deserves emphasis: while consensus expects a supply glut, Variant Perception argues that the risk balance points to significant volatility in 2026. They caution that being contrarian isn’t the goal — rather, the underlying dynamics simply suggest an unusually turbulent year ahead for crude.