Since late October, U.S. stocks have entered a quiet but powerful shift. While the S&P 500 has gone essentially nowhere, the market beneath the surface has been undergoing a major transformation.

Technology stocks — the undisputed leaders of the bull market since late 2022 — have started to lose momentum. In their place, more cyclical areas of the market such as financials, energy, materials, and small-cap stocks have surged ahead.

Wall Street strategists call this a “rotation trade” — a broadening of market leadership after years of dominance by a small group of mega-cap tech stocks tied to the artificial-intelligence boom. Investors, increasingly cautious about crowded trades and lofty valuations in tech, are now hunting for opportunities in parts of the market that have lagged for years.

“We’ve already been seeing a little bit of broadening out,” said David Lefkowitz, head of U.S. equities at UBS Global Wealth Management. “We do think it could maybe even broaden further.”

That shift is starting to show up clearly in the data.

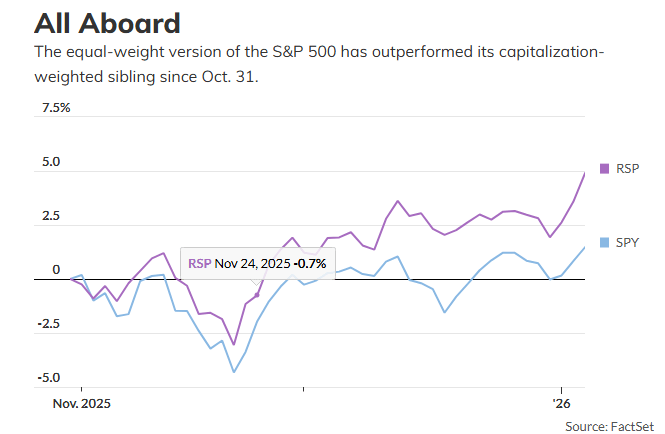

For years, the traditional, capitalization-weighted S&P 500 easily outperformed its equal-weighted counterpart — a sign that a handful of massive tech stocks were doing most of the work. Recently, that relationship has flipped. Since Oct. 31, the Invesco S&P 500 Equal Weight ETF has climbed 4.8%, far ahead of the 1.5% gain in the standard S&P 500 ETF. In other words, the average stock is now beating the giants.

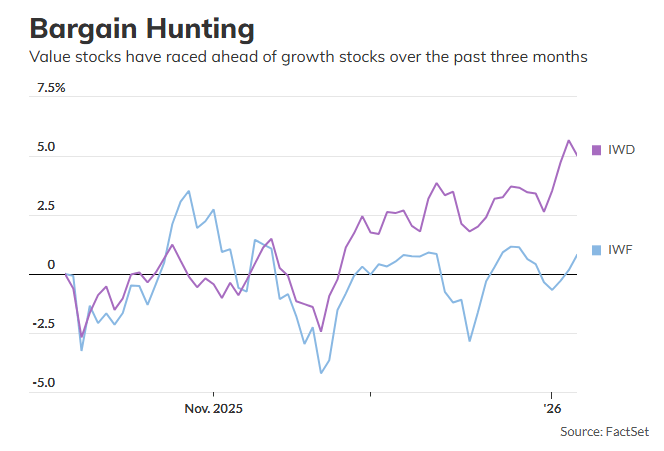

The Dow Jones Industrial Average, which leans more toward value-oriented companies, is also off to its strongest start to a year since 2003. And it isn’t just large caps: Value stocks in the Russell 1000 have been beating growth stocks since October, reversing another long-standing market trend. The Russell 1000 Value ETF is up more than 5% over that period, while the growth version has fallen.

Sector performance tells the same story. Since late October, the S&P 500’s technology sector is down more than 4%, while energy, financials, and materials have surged — with materials up more than 10%. Even communication services, another AI-heavy sector, has continued to rise, but leadership is clearly no longer concentrated in tech alone.

Investors see several forces driving this shift. Expectations are growing that the U.S. economy will remain resilient in 2026, global growth will improve, and inflation will stay under control. That combination favors more economically sensitive, value-oriented sectors. At the same time, markets are betting the Federal Reserve will be able to cut interest rates a few times this year, which would further support small caps and other rate-sensitive areas.

Some strategists believe the market may be heading back toward a “Goldilocks” environment — not too hot, not too cold — similar to the one that powered stocks through much of the 2010s.

“With inflation cooling, the Fed easing and recession risks staying low, 2026 could mark the return of a Goldilocks economy,” said Jack Janasiewicz of Natixis Investment Managers.

That doesn’t mean the AI trade is over. But investors are becoming more selective, separating true winners from hype. The bigger change is that portfolios no longer depend entirely on a few mega-cap tech names to move higher.

Small- and mid-cap stocks are already showing signs of life. Some strategists, including Ed Yardeni, believe they could even outperform large caps in 2026 after years of underperformance — particularly in sectors like financials, industrials, and healthcare.

Importantly, analysts now expect small-cap companies to grow earnings faster than large caps in 2026 — the first time that’s happened since the bull market began in 2022.

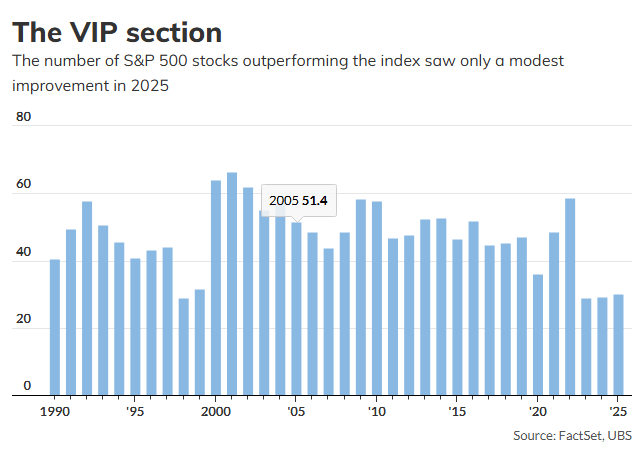

Meanwhile, the concentration problem in the S&P 500 remains extreme. In 2025, the “Magnificent Seven” once again drove roughly 40% of the index’s total return, even though only two of them actually beat the index. Just 30% of S&P 500 stocks outperformed last year, and the top 10 stocks now make up more than 40% of the index’s total value — the highest level in decades.

Valuations make the rotation argument even more compelling.

Despite the recent shift, the S&P 500 still trades at a massive premium: its price-to-earnings ratio is 36% higher than the equal-weight version of the index and nearly 50% higher than the S&P 600 small-cap index.

“There have been plenty of false starts in recent years,” said Michael O’Rourke of Jones Trading. “But if this trend continues, there is a vast valuation gap to close.”

In short, after years of narrow leadership, the U.S. stock market may finally be entering a healthier phase — one where gains are spread more evenly across sectors, styles, and company sizes. For diversified investors, that could be very good news.

About DayTradeToWin

DayTradeToWin® is a professional trading education company with over a decade of experience developing rule-based, non-predictive trading software for the futures markets.

Our methodology is built around structure — not opinions, news, or guesswork. Every strategy is designed to focus on:

- ✔ Market confirmation

- ✔ Risk management

- ✔ Trade timing precision

- ✔ Trader discipline

- ✔ Structured decision-making

We specialize in providing traders with objective tools that remove emotional bias and emphasize consistency over prediction.

DayTradeToWin’s software and educational programs are used by independent traders worldwide seeking a rules-driven approach to futures trading.

Educational Disclaimer

All content, software, training materials, and examples provided by DayTradeToWin are for educational purposes only and do not constitute financial, investment, legal, or trading advice.

Trading futures involves substantial risk and is not suitable for all investors. Past performance is not indicative of future results. Always trade with risk capital and consult a licensed financial professional before making investment decisions.