Don’t Fall for the June Myths: Seasonal Market Investing Patterns Lack Substance

Every June, investors are warned about two familiar — but unsubstantiated — seasonal trends: the dreaded “June swoon” and the hopeful “summer rally.” According to lore, stocks either tank this month or begin a bullish three-month run.

But the data tell a different story. Historically, June is just another month — neither especially weak nor particularly strong. In fact, the Dow Jones Industrial Average has averaged a 0.62% monthly gain since its inception in 1896, and June performs right in line with that.

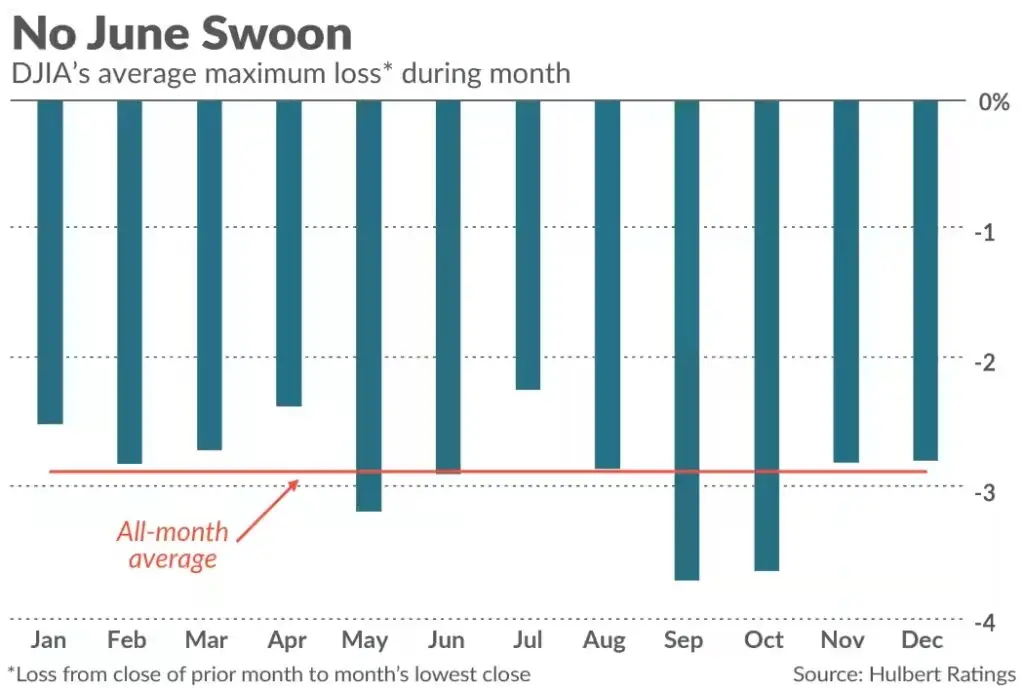

The Myth of the “June Swoon”

While it’s likely the market will dip at some point in June (as it does in most months), the question is whether it dips more often or more severely than usual. The answer is no.

Looking at the Dow’s historical data, the average maximum intra-month loss for June is virtually indistinguishable from the average across all months. Moreover, May, September, and October all show larger average declines. So, despite its catchy name, the “June swoon” doesn’t hold up under statistical scrutiny.

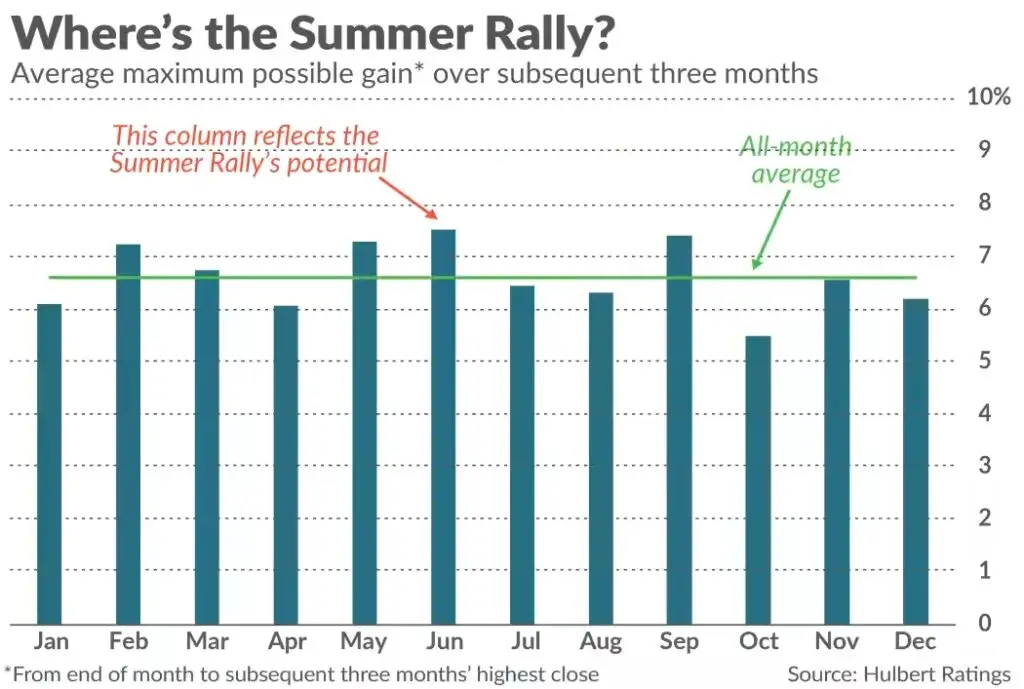

The “Summer Rally” Isn’t Much Better

On the flip side, some investors pin their hopes on a “summer rally,” supposedly beginning in June. To test this, I measured the Dow’s biggest rally from the start of June through the end of August and compared it to similar three-month periods across the calendar.

The result? June’s average summer rally potential is only marginally better — a mere 0.9 percentage points higher — and not statistically significant at the 95% confidence level commonly used to validate real patterns. And even if it were, you’d need perfect hindsight to capture that precise gain.

Bottom Line: Coin Toss Logic

If you’re thinking of adjusting your portfolio based on either of these June-related trends, you might as well flip a coin. Neither pattern has reliable data to support it.

A Lesson in Market Mythology

Even if the June swoon or summer rally did show statistical significance, that alone wouldn’t justify acting on them. Patterns without a solid theoretical explanation are prone to be meaningless coincidences — a classic pitfall for data miners. As David Leinweber illustrates in his book “Stupid Data Miner Tricks,” plenty of statistically “valid” market patterns turn out to be completely spurious.

And don’t waste time trying to reverse-engineer a justification either. As Lawrence Tint, former U.S. CEO of BGI (the creator of iShares), points out: once a pattern’s cause becomes widely understood, the advantage disappears. Investors would rush to front-run the opportunity, and the pattern would vanish.

In essence, seasonal investing patterns like those tied to June live in a state of limbo — either meaningless or quickly arbitraged away. Investors are better off relying on sound strategies grounded in fundamentals rather than market folklore.