Gold deserves up to a 9% slice of a portfolio — precisely because it doesn’t zig when stocks and bonds zag.

As September kicks off, markets look shaky: gold is at record highs while bond yields in the U.S., U.K., and France climb amid political uncertainty. A recent note from hedge fund DE Shaw digs into just how much gold belongs in an investor’s mix, framing it as an “NPSOV” — a non-productive store of value — a category it shares with bitcoin, fine art, and even vintage wine.

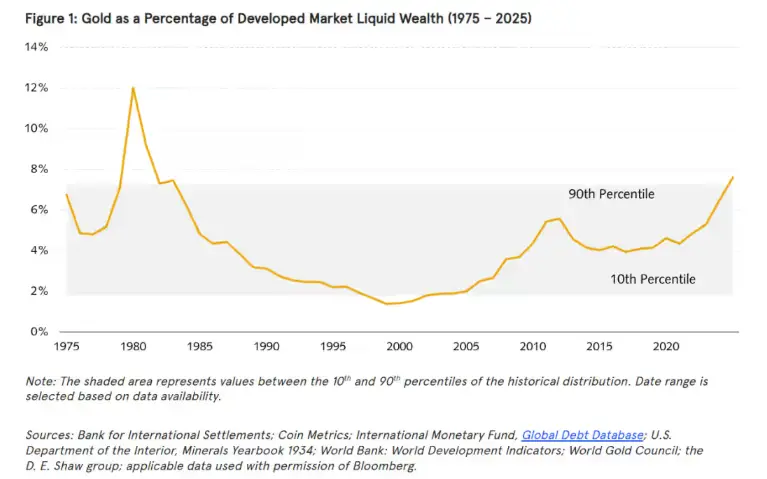

The problem with valuing gold is that it generates no income, has few industrial uses, and could theoretically be worth nothing if society stopped treating it as valuable. Yet history shows it tends to track global wealth growth. Since 1975, it’s typically accounted for 1.8% to 7.3% of developed market liquid wealth — though today it’s breaking out of that range.

DE Shaw’s analysis assumes global wealth grows faster than GDP (as it has over the past 50 years), and that gold supply expands about 1.6% annually. Putting the pieces together, the firm estimates gold’s return at just 0.5% above inflation-adjusted risk-free rates, with volatility around 15%. Hardly thrilling on its own.

But here’s the kicker: gold’s real value lies in diversification. Its long-term correlations with stocks, bonds, and inflation are weak, giving portfolios protection when traditional assets move in sync. In fact, the more stocks and bonds move together, the more useful gold becomes.

DE Shaw’s conclusion:

- If stock-bond correlations are negative → gold’s optimal allocation is ~6.5%

- If stock-bond correlations are positive → gold’s allocation jumps to ~9%

Right now, correlations are sitting near zero — leaving gold’s sweet spot somewhere in between.