Valuations Surge to Extreme Levels as Market Enters Historically Weak Season

U.S. stocks have stumbled since the start of August, and several Wall Street strategists warn this may signal the beginning of a deeper correction.

Julian Emanuel, chief equity and quantitative strategist at Evercore ISI, expects a market pullback of 7% to 15% by mid-October, according to a note shared with MarketWatch. Analysts at Deutsche Bank echoed similar caution, forecasting a milder retreat but acknowledging near-term risks.

Still, there are silver linings. Emanuel believes the broader bull market remains intact and that any deeper selloff could draw in dip buyers. He advises investors to avoid panic-selling and instead consider portfolio hedges to manage short-term volatility.

Valuations Back in “Nosebleed” Territory

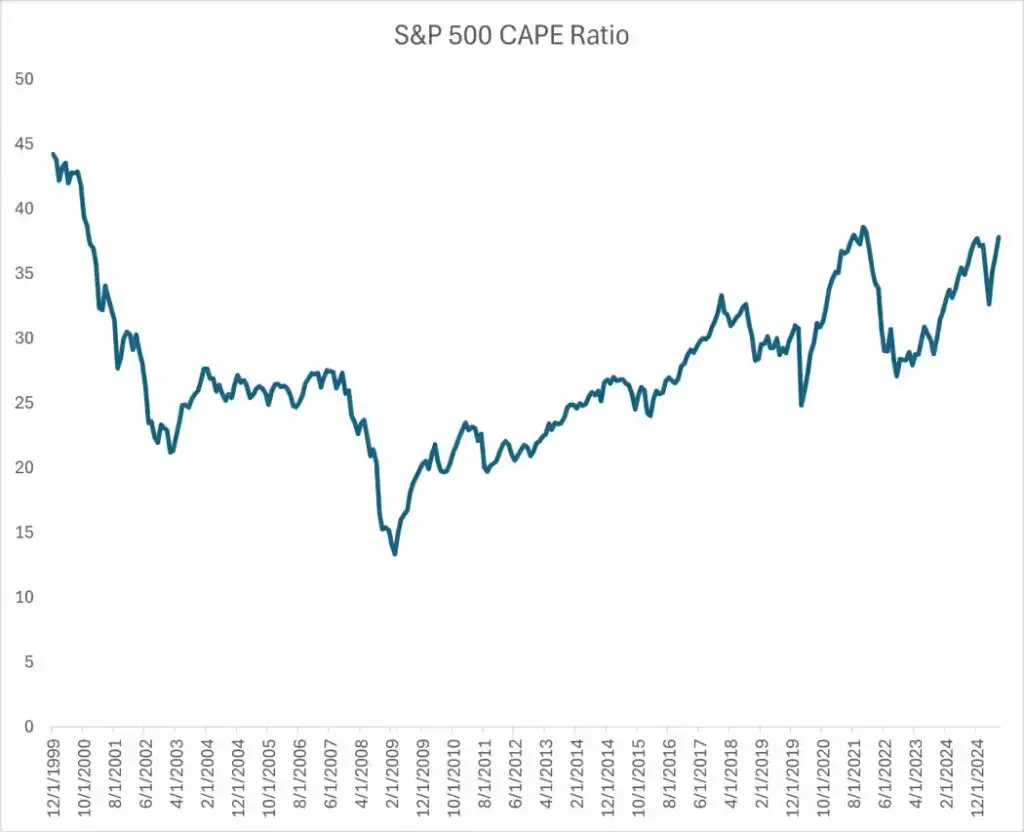

The cyclically adjusted price-to-earnings (CAPE) ratio, popularized by Yale economist Robert Shiller, climbed above 38 in late July — its highest since late 2021.

That previous peak preceded one of the toughest market years in decades, as the Federal Reserve launched an aggressive interest-rate hiking campaign that led to the S&P 500’s worst annual performance since 2008, per FactSet data.

While Emanuel doesn’t foresee a repeat of 2022, he warns that elevated valuations make stocks more sensitive to negative surprises.

Seasonal Weakness on the Horizon

Historically, the August-to-October period is the weakest stretch of the year for equities, according to BTIG’s Jonathan Krinsky.

Although the relative strength index (RSI) has eased from overbought levels, it remains elevated, suggesting the current pullback could have further to go, said Mark Hackett, chief market strategist at Nationwide.

Wall Street’s “Fear Gauge” Creeps Higher

The Cboe Volatility Index (VIX), widely viewed as Wall Street’s fear gauge, has rebounded from its lowest reading since January. Emanuel notes this move likely reflects mean reversion — a sign that volatility could continue rising in the near term.