Foreign Pullback From U.S. Stocks Won’t Last, Says JPMorgan

Retail investors have been the engine behind this year’s market rally — and they’re not done yet.

That’s the core message from JPMorgan strategists in their latest outlook, which forecasts a major wave of retail-driven inflows into U.S. equities over the second half of 2025. Led by Nikolaos Panigirtzoglou, the team expects around $500 billion in total equity inflows to help push stocks up another 5% to 10% by year-end.

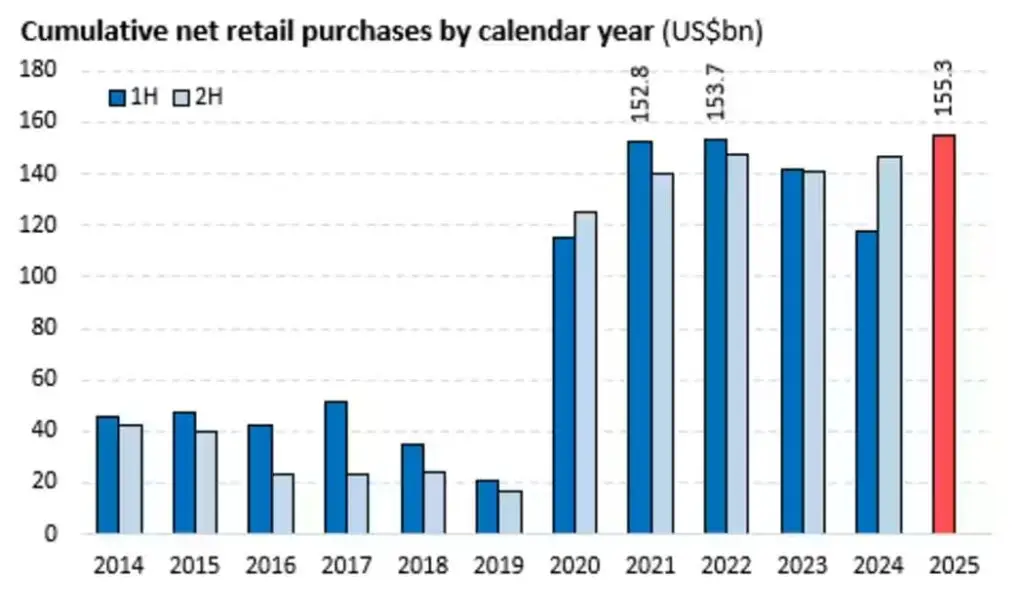

Of that, about $360 billion is expected to come from retail investors, who had stepped back in May and June to lock in gains after aggressive dip-buying in March and April. This pause, they argue, was profit-taking — not a sign of fading enthusiasm. “We believe retail investors will resume buying and help propel the market starting in July,” the strategists wrote.

Other buyer groups may offer less support. Hedge funds, which increased exposure earlier in the year, are seen as near their limit. Quant-driven funds pulled back in May and June, and could return later in the year. Meanwhile, pension funds and insurers are expected to remain net sellers, shifting further into fixed income, with projected equity outflows of $360 billion for 2025.

However, the wildcard might be foreign investors. Since February, global flows into U.S. equities have slowed dramatically — what JPMorgan calls a temporary “boycotting.” But that isn’t likely to last. “Foreign investors can’t ignore the world’s top growth engine — the S&P 500 and the Magnificent 7,” the strategists said.

What’s holding them back? Currency risk. The weaker U.S. dollar has deterred overseas buying, but signs of stabilization are emerging. The ICE Dollar Index (DXY) is hovering near April lows around 98. If the dollar firms up, JPMorgan estimates foreign buyers could return with $50 billion to $100 billion in flows.

All told, this renewed demand — driven primarily by retail — could power markets higher into year-end.