The “midterm curse” suggests the ruling party is likely to struggle — and market often wobble with it.

Most American families probably tried to steer clear of politics over Thanksgiving. Investors, however, don’t have that luxury. With the 2026 U.S. midterm elections approaching next November, markets are already preparing for another cycle of political uncertainty.

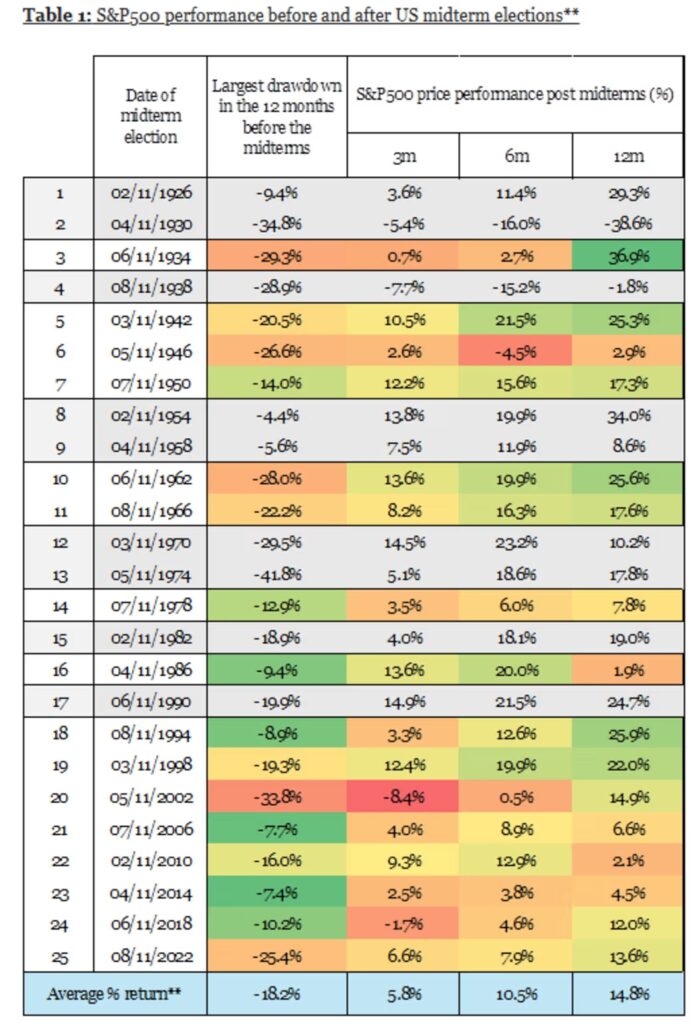

Harry Colvin, senior market strategist at Longview Economics, examined a century’s worth of data to understand how midterms tend to affect stocks. His findings point to a surprisingly consistent pattern.

According to Colvin, the S&P 500 typically suffers a sizable drawdown in the 12–18 months leading up to a midterm election — often a sharp drop that ultimately becomes a buying opportunity. After the vote, equities have historically delivered strong gains over 3-, 6-, and 12-month periods.

Why the pre-election turbulence? Investors dislike uncertainty, and midterms can threaten policy clarity, raise the risk of gridlock, and cast doubt over the economic outlook. Once the election passes, however, that uncertainty clears and markets can refocus on fundamentals with a clearer sense of the policy path ahead.

This cycle carries its own twist. Supporters of the Trump administration’s agenda may be particularly sensitive to the outcome, given that midterms rarely favor the sitting president’s party. Historically, the president’s party tends to lose congressional seats — especially in the House — a trend known as the “midterm curse.” Drivers include voter fatigue, higher turnout from the opposition, and early-term policy dissatisfaction.

Colvin cautions that historical analysis has its limits. Markets usually see one or two pullbacks a year anyway, and not all are tied to elections. Some midterms have also occurred around recessions, muddying the signals. Of the 25 midterms over the last century, nine took place within a year of a recession and were excluded from his study.

Of the remaining 16, twelve were preceded by S&P 500 pullbacks of more than 10% in the year before election day. Seven of those drops were 20% or more; five were in the 10–20% range.

And those declines generally set the stage for solid market rebounds. On average, the S&P 500 gained 5.8% in the three months after the midterms, 10.5% after six months, and 14.8% after a year. Larger pre-midterm drops tended to lead to stronger 12-month recoveries, though the relationship is not exact.

Overall, Colvin believes any volatility before the 2026 midterms is likely to be a buying opportunity — assuming the U.S. avoids recession, as Longview currently expects. “We are overweight U.S. equities in our tactical portfolio,” he says.