Goldman Sachs Stays Bullish on Gold — Even After Its Steep Drop

For investors tired of the endless AI chatter, this week’s gold selloff has shifted the spotlight — and reignited debate.

After suffering its biggest one-day drop in more than a decade on Tuesday, it’s next move has become the hot topic: can it rebound and push higher? Goldman Sachs thinks so. The bank is holding firm on its end-2026 price target of $4,900 per ounce, citing upside risks from central bank and institutional demand.

“The speed of recent ETF inflows and client feedback suggest many long-term allocators — including sovereign-wealth funds, central banks, pension funds, and asset managers — are preparing to boost gold exposure as a strategic portfolio diversifier,” analysts Lina Thomas and Daan Struyven wrote in a note.

That optimism echoes a separate bullish call from JPMorgan, where strategists led by Nikolaos Panigirtzoglou argue that gold prices could more than double within three years as investors increasingly use it to hedge equity risk.

According to the team, the recent it plunge wasn’t triggered by retail investors but rather commodity trading advisers taking profits on gold futures. Futures prices have surged 56% this year, and the strategists say most retail buyers of gold ETFs remain in for longer-term reasons.

Their analysis suggests that today’s gold buying isn’t just a “debasement trade” driven by fears of a weaker dollar. Instead, it reflects a shift toward using gold to hedge stock exposure, especially as investors continue to buy both equities and gold while avoiding long-term bonds — their traditional hedge.

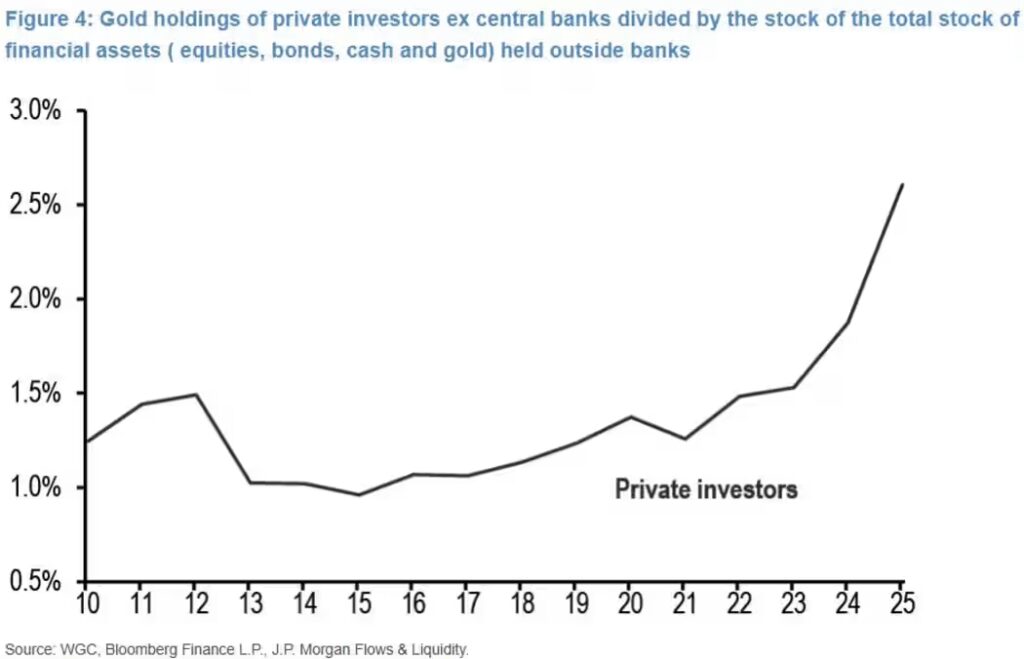

Globally, nonbank investors have lifted their gold allocation to 2.6% of holdings, JPMorgan estimates. But if investors are indeed replacing bonds with gold to offset stock risk, that allocation could still be too low.

The strategists note that when longer-dated bonds failed to protect portfolios during market turmoil following President Trump’s tariff announcements, many investors began reassessing gold’s role. Replacing even 2% of bond holdings with gold, they calculate, would lift gold’s share of total assets to 4.6% — a shift that could nearly double gold prices.

Looking ahead, if equity allocations rise to dot-com era levels and global financial assets expand as expected, gold would need to climb 110% by 2028 to reach that new equilibrium.

In short, Goldman and JPMorgan see it not as a relic, but as a comeback hedge for a new market era — one where central banks, funds, and everyday investors may all be racing to own more of it.