Several indicators on Wall Street are flashing sell signals, warns Longview Economics.

Despite weakness in tech dragging stocks lower this week, the S&P 500 finished the prior session just 1.5% below its August 14 record. That resilience might tempt some to dismiss recent choppiness as noise within a broader uptrend. But Chris Watling, CEO and chief market strategist at Longview, says caution is warranted heading into September — a historically difficult month for equities.

“You get warning shots before you get meaningful pullbacks,” Watling told MarketWatch, outlining a series of red flags now emerging.

Among his concerns:

- Low trading volumes suggest investors are already fully invested — a condition that has often preceded market declines.

- Valuation froth is building, with more than 20% of stocks trading above 10 times enterprise value-to-sales, echoing the peaks of 2000 and 2021. Palantir’s sharp rally is, in his view, an example of “overcrowded sexy stocks.”

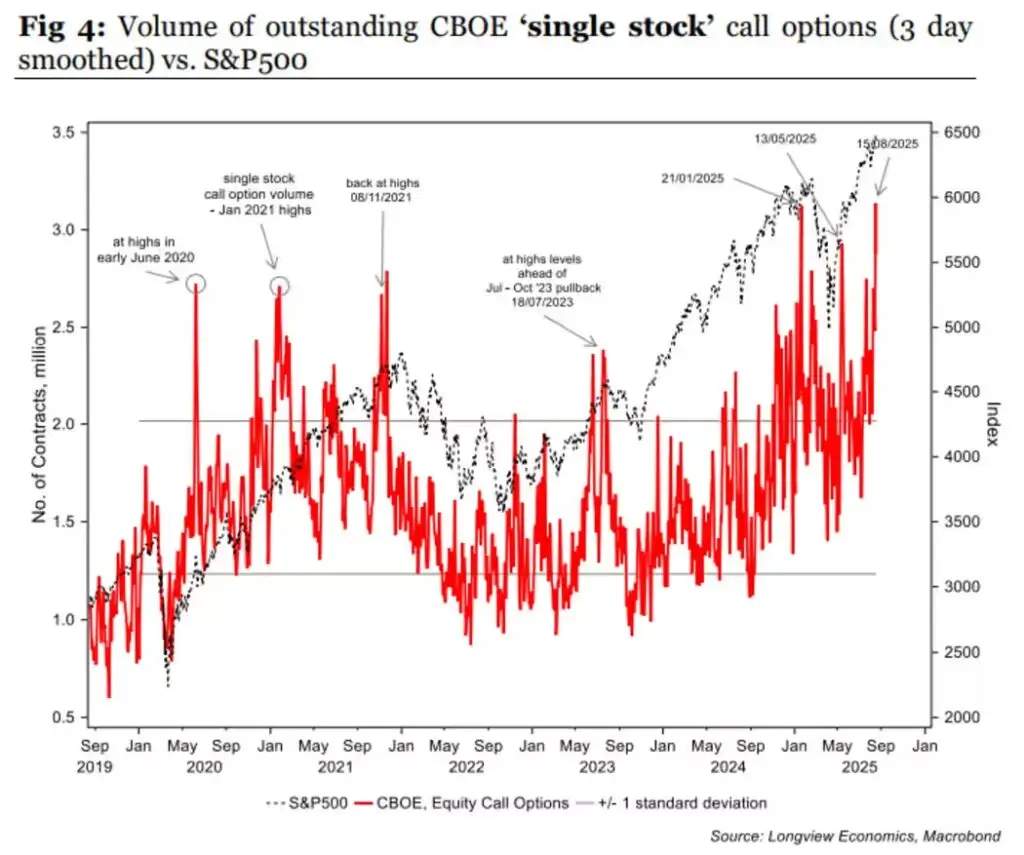

- Options speculation has surged, with single-stock call option volumes hitting five-year highs, consistent with retail-driven risk-taking and the return of meme-stock behavior.

- Margin debt is rising, while corporate bond spreads remain extremely tight, reflecting heightened complacency.

- Volatility signals also look troubling: the steep curve in VIX futures combined with Longview’s valuation-to-volatility model are both on “sell.”

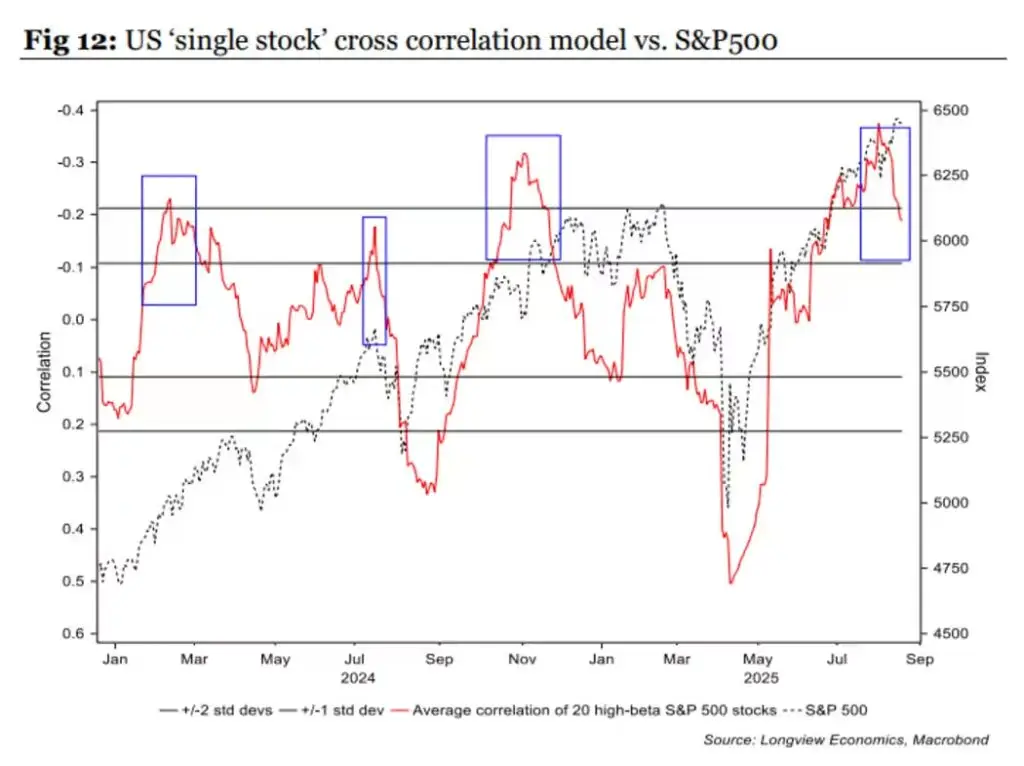

Additional models at Longview — from sector correlations to equity-versus-bond relative value — are also pointing to a potential pullback. Watling further highlights liquidity risks, noting that Treasury issuance is now draining traditional market liquidity as the Fed’s reverse repo facility nears exhaustion.

Even so, Watling isn’t outright bearish. He stresses that he wouldn’t recommend shorting equities unless a bear market was clearly underway, something unlikely while the Fed remains on hold. Aggressive rate cuts, he adds, would likely fuel another rally in the near term.

For now, he calls himself “tactically neutral” on U.S. equities, with a preference for healthcare and staples in a cautious environment. If the Fed pivots to faster cuts, however, he would tilt toward cyclical sectors.