A “Good” S&P 500 Valuation May Be a Bad Omen for Future Returns

Markets paused on Wednesday as investor focus shifted from geopolitical concerns to upcoming economic data, interest rates, and tariff developments. A flood of economic reports due in the next two days could shape short-term market direction.

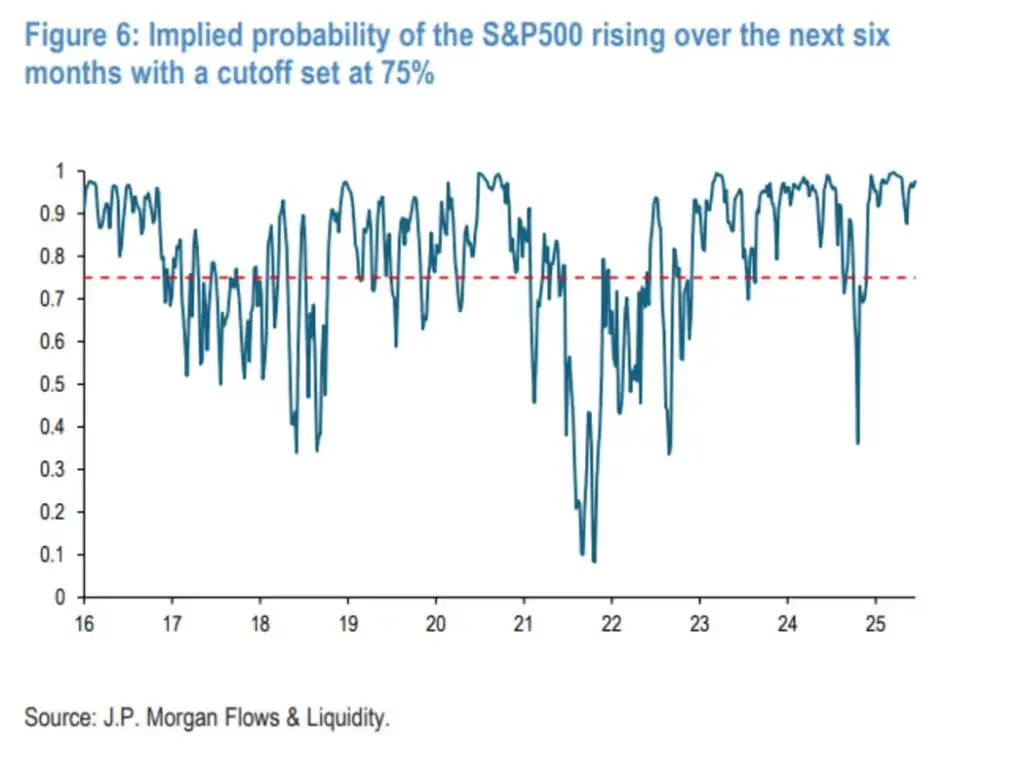

But it’s not just data that drives the market. JPMorgan strategists led by Nikolaos Panigirtzoglou have developed a model to predict the S&P 500’s trajectory over the next six months. It analyzes six key signals — volume, valuation, investor positioning, fund flows, economic momentum, and price momentum — each measured against its historical norm using z-scores.

Trained on data through late 2022 and tested on more recent periods, the model was especially geared to predict market declines — since a buy-and-hold stance would have been right over 90% of the time historically. The model correctly predicted six-month down moves 76% of the time in training, and 63% in out-of-sample testing — outperforming competing models, which especially struggled to forecast downturns.

Key findings reveal that:

- Stronger economic momentum (measured by changes in the global manufacturing PMI) and higher trading activity typically signal a rising market.

- Heavy bullish positioning and strong fund inflows into stocks versus bonds point to overcrowding — often preceding a market pullback.

- When equity momentum far outpaces bond market momentum, it’s also a red flag.

But perhaps the most surprising insight: Better valuations tend to predict lower future returns. JPMorgan suggests this is because valuations often track movements in the 10-year Treasury yield — and falling yields may signal deteriorating growth expectations.

As for the present outlook? The model currently estimates a 96% probability the stock market will rise over the next six months.