HSBC: Market Underestimating Earnings Ahead of Q2 Season

As the second-quarter earnings season kicks off, HSBC strategists argue that expectations are set far too low — setting the stage for upside surprises.

Despite ongoing uncertainty around U.S. trade policy, markets appear less rattled than before. “The tariff debate has faded into the background with the U.S.-China trade pause,” says Max Kettner, HSBC’s chief multi-asset strategist. He notes that markets are showing reduced sensitivity to tariff headlines.

Economic fundamentals are also holding up well, particularly consumer spending, which has rebounded. HSBC believes consensus estimates are overly pessimistic. “Low forecasts lower the bar for positive surprises, which can drive upward revisions and act as a catalyst for risk assets,” Kettner explains.

Concerns about inflation from tariffs haven’t materialized either — in fact, price pressures appear to be easing. HSBC also sees a silver lining in tariffs: they help keep investor sentiment and positioning more balanced.

As for corporate earnings, HSBC challenges the widely held view that Q2 will show a sequential drop. “We disagree,” the team says. “Earnings estimate cuts over recent months are the steepest in three years, and front-loaded economic activity should lead to at least a temporary earnings bump — not a decline.”

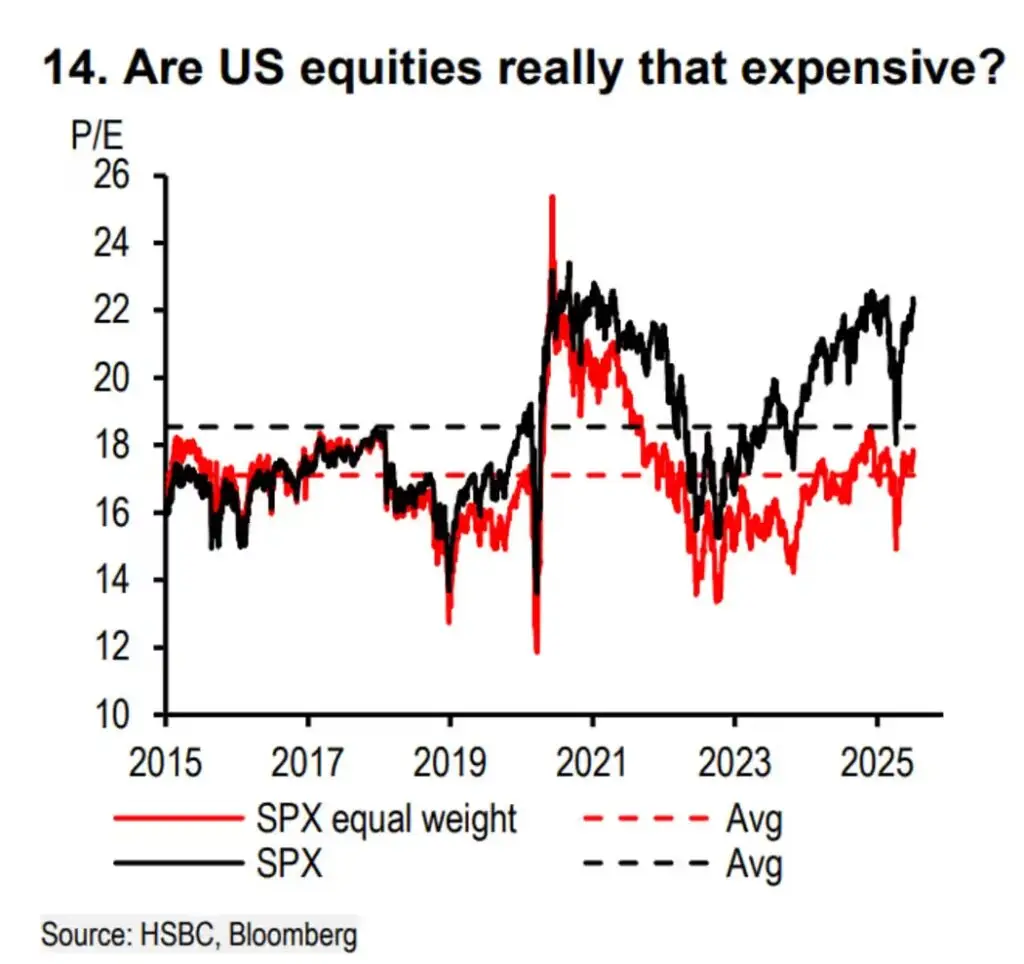

And what about valuations? While some argue the market is stretched, HSBC counters that the equal-weighted S&P 500 is only slightly above its long-term average — hardly excessive.

In short, HSBC sees widespread bearishness on the U.S. — whether it’s expectations for slower growth, a weaker dollar, or underperformance in equities — as overdone.

Reflecting this view, HSBC has increased its overweight on U.S. stocks by 4 percentage points, now making up 31% of its recommended multi-asset portfolio. Overall, equities comprise 50% of the mix, followed by government bonds (25%), corporate credit (10%), commodities (5%), and cash (5%).