Market May Face ‘Sell-the-News’ Reaction Despite Trade Progress, Warns Sevens Report

According to Sevens Report Research, the recent rally in U.S. stocks could lose steam—even if trade negotiations yield positive outcomes. The market has already priced in a significant rollback of the sweeping “liberation day” tariffs announced by President Donald Trump on April 2, raising the risk of a “sell-the-news” reaction once trade deals are officially confirmed.

“The Trump administration has substantially walked back the April 2 tariffs,” noted Tom Essaye, founder and president of Sevens Report Research, in a Monday update. He cited delays in implementation and exemptions on major import categories such as semiconductors, electronics, pharmaceuticals, and a utomobiles as evidence of this shift.

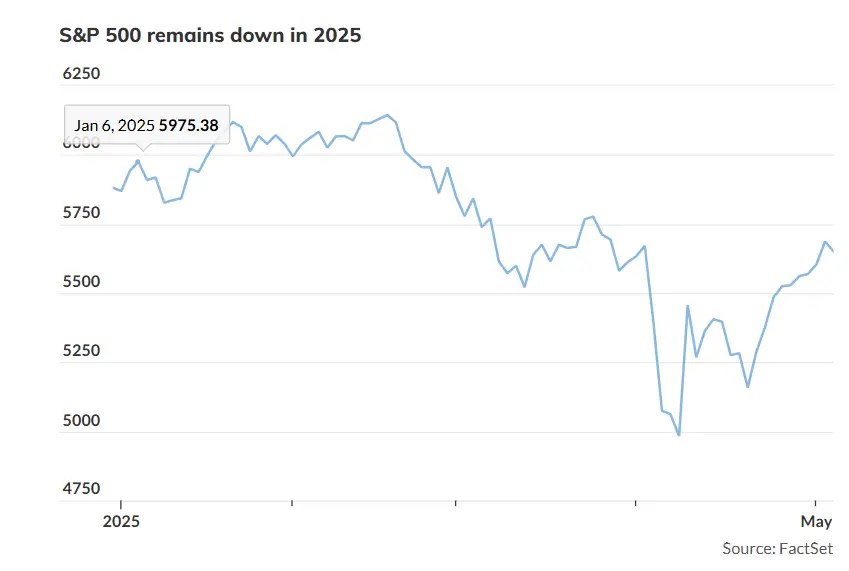

Despite a nine-day winning streak that ended Friday, the S&P 500 slipped 0.6% on Monday to close at 5,650.38, per FactSet. The rally had helped erase earlier losses triggered by tariff fears, but Essaye remains cautious.

“While the past month hasn’t been as bad as initially feared, I don’t believe the current developments are strong enough to push the S&P 500 sustainably higher,” Essaye said, reiterating his outlook for the index to remain in the 5,100–5,500 range.

Investors remain wary that elevated tariffs could weigh on economic growth and raise consumer costs. With the White House pausing the reciprocal tariffs and trade negotiations ongoing—particularly with China—markets have responded positively to signs of easing tensions. Yet Essaye warns the risk of disappointment still looms.

“Tariffs will still end up significantly higher than they were at the start of the year, and that’s a headwind for growth,” he said. “At this point, the market is vulnerable to any negative surprises on the trade front.”

Even with recent gains, the S&P 500 is still down 3.9% year-to-date, following its third consecutive monthly decline in April. Broader indexes, including the Nasdaq Composite and the Dow Jones Industrial Average, also ended Monday in the red.

“Economic data has held up, but we haven’t yet seen the real economic impact of tariffs and related uncertainty,” Essaye added. “Like with earnings, the risk to growth remains tilted toward the downside.”

As a result, Essaye continues to favor more defensive areas of the market such as utilities, consumer staples, and healthcare. He also advocates for broad diversification, highlighting the Invesco S&P 500 Equal Weight ETF (RSP) as a preferred vehicle. For risk-conscious investors, he recommends low-volatility funds like the iShares MSCI USA Min Vol Factor ETF (USMV) and high-quality exposure through the iShares MSCI USA Quality Factor ETF (QUAL).

“Yes, the market has enjoyed a rebound, and events since early April weren’t as bad as feared,” said Essaye. “But ‘not as bad’ doesn’t mean ‘good,’ and I believe current price action is assuming fundamentals are stronger than they actually are.”