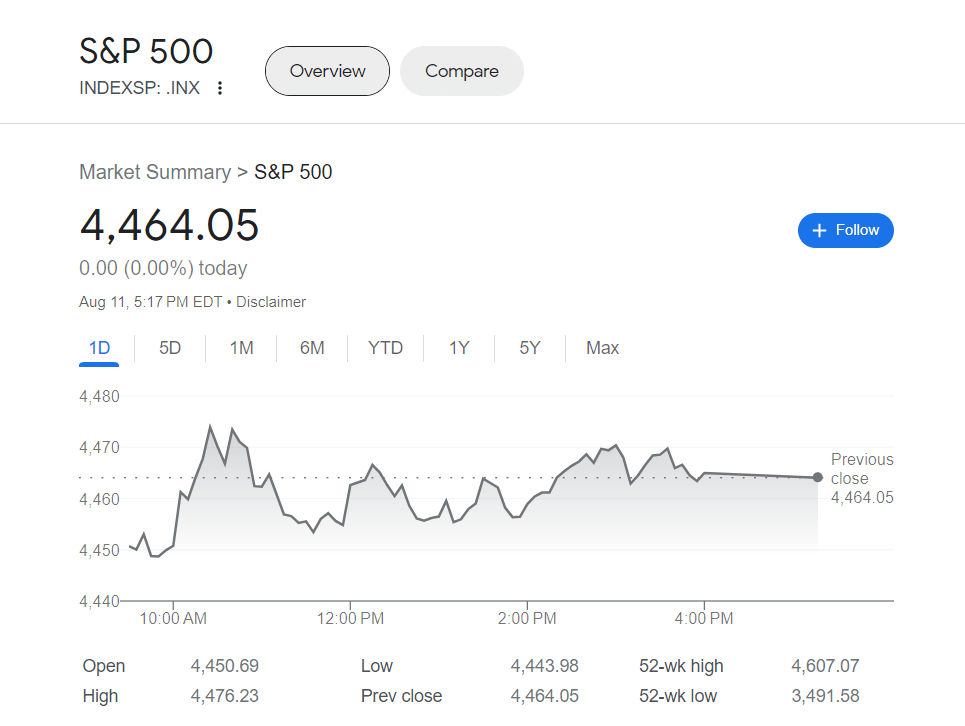

Historical evidence has proved that August and September are often times of turbulence in the American stock market. Thus the first weeks of the month having turbulence should not be an unexpected occurrence. As the S&P 500 index spiked 20% from January to July 2023 many investors have been wanting the market to stabilize after such a steep rise. As of the closing of the market on Friday it is up 25% from its post-bear market minimum of 3,577.03 on October 12.

What could potentially derail the 2023 rally?

To understand the rally it is beneficial to consider why it has occurred. According to Mark Hackett the Principal of Investment Research at Nationwide the rally has been due to the lack of actualization of worries that had previously been held.

I would suggest that around ninety percent of the changes we have observed in the past ten months have been a return to a less fearful mindset Hackett stated to MarketWatch in a phone interview.

In October 2022 the Federal Reserve increased the Fed-Funds rate drastically by 75 basis points while inflation had decreased from its June peak above 9%. People were expecting an incoming recession making the situation alarming.

Tom Essaye the initiator of Sevens Report Research argues that the resurgence has been built on three main beliefs: investors now perceive that the Federal Reserve is probably done or almost done increasing the rates of interest; it looks like the economy should possibly avert a recession completely; and inflation has stayed generally stable.

If economic data were to weaken causing a downturn in the market there would be trouble. Additionally if core inflation slowed down or increased or if Federal Reserve Chair Jerome Powell implied another interest rate hike is inevitable which would drive up Treasury yields it would be problematic.

Essaye noted in a note last week that if this scenario were to play out it would greatly weaken the three foundations of the rally so investors ought to anticipate a major decrease in stocks notwithstanding the recent retreat. He further remarked that in the event of this occurence a drop of over 10% could be expected potentially negating most of the increase of stocks since June and potentially even all of the gains made this year.

That scenario has yet to materialize.

Compared to last year the US consumer price index showed an increase of 3.2% in July from 3% in June as reported last week. On the other hand the core rate which does not include food and fuel prices was observed to slow down to 4.7% from 4.8% The July producer price index which records costs in the wholesale market was a bit better thanticipated but investors still believe that the Federal Reserve will maintain its rate when they meet in September.

Policy makers are expecting to be presented with yet another set of jobs data inclusive of the August employment report and the inflation figures prior to their upcoming meeting.

At the same time a sudden surge in Treasury yields with the 10-year note interest rate going above 4.15% after reaching its highest point since 2023 near 4.2% recently is causing the stock market to stay weak. Bond yields increasing can makegovernment bonds more appealing than other investments and can also drive up the expenses for businesses to borrow money.

Stocks have increased in price since the end of last year as the worries which had been factored into the market eventually did not turn out to happen but this trend is now over.

As the market rally was set off by a prevalence of a negative outlook hopes of a perfect combination of controlled inflation a restrained Federal Reserve and a thriving economy often referred to as a “Goldilocks” situation could lead to difficulties for optimists according to Hackett. While these expectations don’t appear to be overly high at this point in time they remain worth keeping an eye on.

At the same time investors are worried by seasonal trends. The S&P 500 has historically been relatively sluggish in August according to stats provided by Dow Jones Market Data. Going all the way back to 1928 it has generated an average increase of 0.67% That puts August in fifth place for lowest gain of the S&P 500. September follows in last place with an average drop of 1.1%

Since 1986 the Dow Jones Industrial Average has consistently performed poorly in the month of August with an average return of negative 0.8% Prior to this August was the best month for the blue-chip gauge.

And then there’s volatility.

He suggested that trying to be overly clever with the market is not ideal as it is likely experiencing a normal period of consolidation. He asserted that it is not going to endure a lengthy period of distress.