An expert strategist who accurately predicted the 2023 market rally now foresees a period of stagnation for stocks throughout the remainder of this year and possibly into 2024. This projection stems from a belief that corporate earnings growth will fall short of the overly optimistic expectations set by Wall Street.

Barry Bannister, an equity strategist at Stifel, shared his insights in a recent report, highlighting that the impetus behind this year’s rally – the relief that a U.S. recession wouldn’t materialize in 2023 – has likely reached its zenith.

Bannister’s outlook positions the S&P 500 index to tread a sideways path for the remainder of 2023, eventually concluding around 4,400 points, approximately 68 points lower than its Wednesday closing value, as per FactSet data. Despite this, Bannister identifies potential opportunities within sectors that have lagged behind the market leaders.

His strategy revolves around “pair trades,” involving the shorting of Big Tech stocks while simultaneously buying into financials, materials, industrials, and other cyclical growth stocks that have experienced underperformance.

Bannister further anticipates that the equal-weighted S&P 500 index will outperform the traditionally capitalized S&P 500 in the latter half of the year.

Recent trends have already begun to validate these predictions. In the span since mid-July, coinciding with the start of the corporate earnings season, the equal-weighted S&P 500 has surged by 2.4%, surpassing the 1.6% gain achieved by the conventional S&P 500.

In the same time frame, several members of the “Magnificent Seven” group of mega-cap technology stocks, which Bannister advises shorting, have shown signs of retreat. Apple Inc. and Tesla Inc. have experienced notable declines, while Nvidia Corp. remains relatively steady.

Bannister’s forecasting acumen holds weight due to his prescient call on this year’s market rebound. While many analysts projected a decline in stocks during the first half of 2023, with a subsequent recovery later in the year, Bannister defied convention by predicting a reversal, rooted in the expectation of receding U.S. inflation.

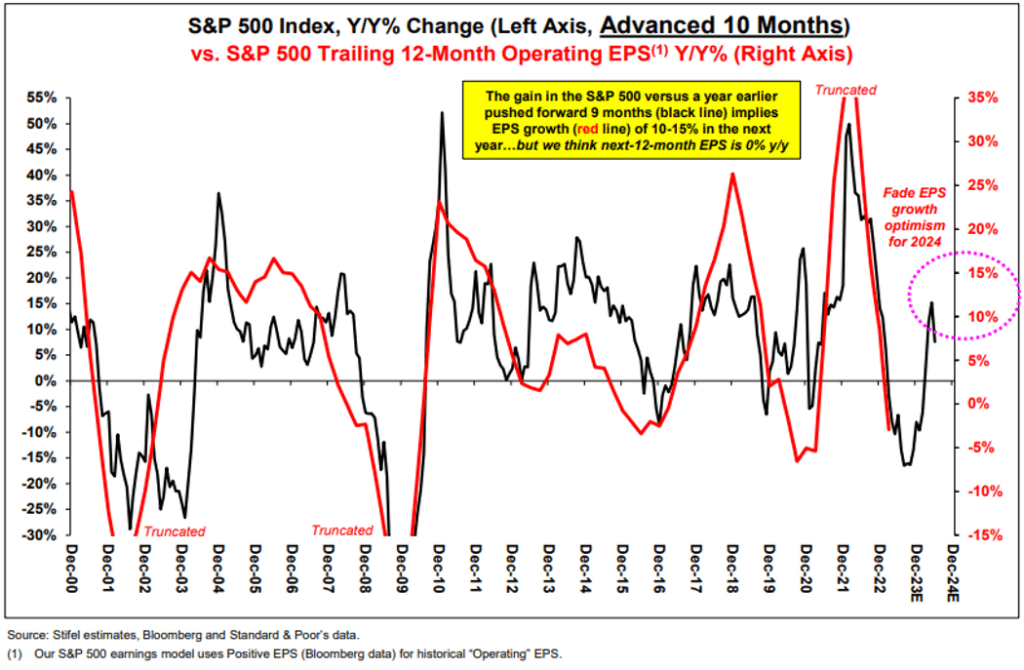

This outlook was vindicated as June’s Consumer Price Index (CPI) data revealed a mere 0.2% rise in consumer prices, indicating inflation’s retreat to a pace not witnessed in two years. Bannister now maintains that the deceleration in inflation is nearing its limit. Moreover, he contends that stocks could face difficulties in 2024 due to Wall Street’s lofty projections for corporate earnings growth being unmet.

For the upcoming year, Bannister and Stifel anticipate aggregate S&P 500 earnings per share to hover around $209, barely diverging from the 2023 projections, as opposed to the market consensus of $226.

Bannister conjectures that earnings could stumble as a mild recession potentially arrives in Q1 2024. Additionally, rising oil prices might yield a minor price shock, pushing the current 3% inflation to a new baseline. This scenario would render it challenging for the Federal Reserve to justify interest rate cuts.

Sluggish economic growth and the aftermath of COVID-19 stimulus measures will also cast a shadow on corporate profits, according to Bannister.

As the markets recently exhibited a downtrend in early August, with the S&P 500, Nasdaq Composite, and Dow Jones Industrial Average all experiencing losses, Bannister’s cautionary stance continues to gain attention.