Critical Insights for the U.S. Trading Day

As the curtain falls on 2023 for Wall Street, Friday marks the final trading day, with the S&P 500 index bulls poised for a potential record high, akin to a football team needing that one decisive push. Tom Lee, Head of Research at Fundstrat, offers a reassuring outlook, asserting that even if the new high eludes today’s trading session, it’s likely to materialize in January.

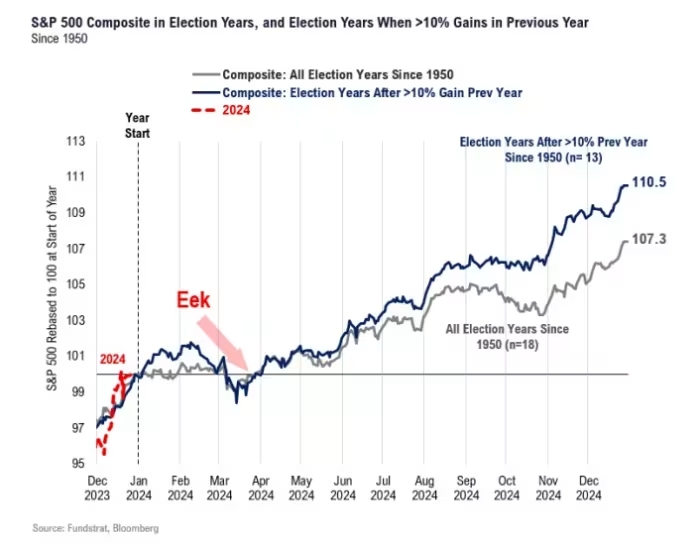

Lee underscores the rarity of a market sharply falling, rebounding to its previous peak, and then experiencing a substantial retreat. Citing data since 1950, he notes that in the 11 instances where the S&P 500 fell 20% and then nearly reached its prior all-time high, the index promptly made an all-time high in every case. The median time for achieving this record was seven days, potentially extending to 20 days, hinting at new highs in January 2024.

While Lee anticipates further market gains, projecting a median max gain of +22% over the next 18 months, he issues a cautionary note. Drawing from historical patterns, he highlights that seven out of the 11 instances involved market consolidation with modest pullbacks, typically ranging from 2% to 5%, potentially bringing the S&P 500 down to the 4,400-4,500 range.

Lee outlines four potential reasons for a pullback this time. First, market impatience could arise while awaiting the Federal Reserve to initiate interest rate cuts. This impatience may intensify if there are signs of central bank officials expressing uncertainty about easing policy, a move the market anticipates in March.

Second, a potential delay in big technology companies benefiting from AI revenues due to what Lee terms a “systemic hack by malevolent AI” could impact the timeline.

Third, Lee attributes the need for market consolidation to the “parabolic gains” witnessed in late 2023, with the S&P 500’s relative strength index staying above the overbought threshold of 70.

Finally, Lee suggests that a market pullback in February to March aligns with historical patterns seen in election years.

Despite these considerations, Lee remains optimistic about the prospective drawdown, aligning with his forecast that the bulk of the market’s gains will manifest in the second half of 2024, ultimately propelling the S&P 500 to 5,200.

Additionally, he anticipates small-caps to rally through the broader market downturn, projecting a 50% jump in the iShares Russell 2000 ETF next year, citing falling interest rates, a dovish Fed, improving economic momentum, and an upturn in housing as contributing factors.