Will we actually see the anticipated cuts in 2024?” George Catrambone, head of fixed income for the Americas at DWS Group, questioned during a phone interview as markets reacted to a stronger-than-expected inflation report on Wednesday. Concerns arose among investors about whether this data might dissuade the Federal Reserve from implementing any interest rate cuts throughout the year.

The March inflation figures, revealed by the consumer-price index, exceeded expectations, sparking worries that inflation might not steadily decline towards the Fed’s 2% target. Consequently, traders swiftly discounted the possibility of rate cuts during the Fed’s June and July meetings, as indicated by the CME FedWatch Tool.

Catrambone observed that the inflation report has made it harder for investors to predict when the Fed might initiate reductions in its benchmark rate. September, previously viewed optimistically for a potential quarter-point cut, now appears uncertain, with the market’s hopes for looser monetary policies being pushed further out.

To curb inflation, which has moderated since its peak in 2022 but remains persistent, the Federal Reserve has maintained its policy rate at an elevated level.

The consumer-price index showed a 0.4% increase in inflation in March, translating to an annual rate of 3.5%, with core inflation, excluding food and energy prices, rising by 0.4% last month, resulting in an annual pace of 3.8%.

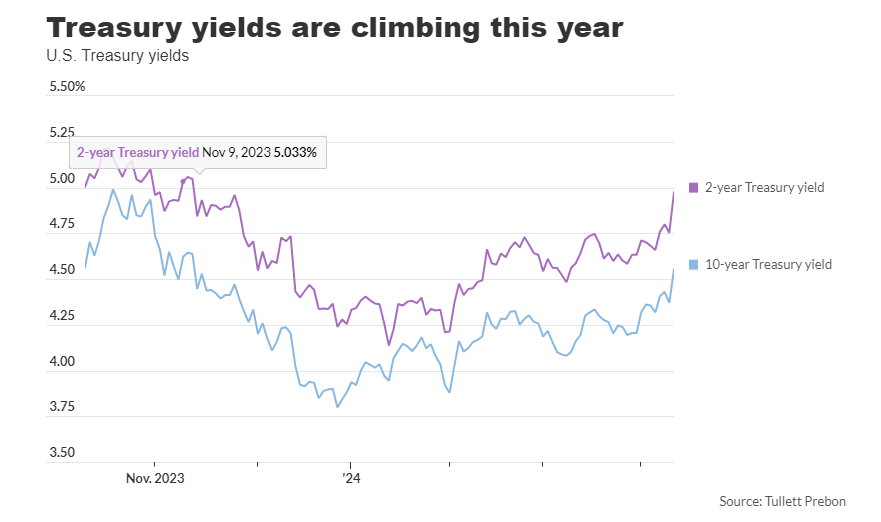

Following the CPI report, Treasury yields surged, with the 10-year Treasury note yield rising approximately 18 basis points to around 4.54%, and the two-year Treasury rate increasing about 21 basis points to around 4.95%, according to FactSet data.

Catrambone anticipates continued market volatility as investors closely monitor economic data and Fed statements until rate cuts become a reality. There’s a risk that rate cuts might not materialize at all this year.

Current market sentiment, reflected in fed-funds futures, suggests expectations that the Fed will maintain its benchmark rate at the current target range of 5.25% to 5.5% during its June meeting, with a 59% probability of the same in July. However, the likelihood of a quarter-point rate cut in September stands at 45.5%.

In the interim, Catrambone foresees investors favoring cash allocations in their portfolios, potentially leading to continued accumulation of money-market fund assets.

While some investors might view the bond market selloff as an opportunity, Catrambone advises caution, particularly regarding long-term Treasurys, which have faced pressure this year due to shifting rate-cut expectations.

He suggests exploring buying opportunities in areas such as the safest portions of collateralized loan obligations (CLOs), with AAA-rated slices offering yields of nearly 6%.

Despite the stock market‘s sharp decline on Wednesday, John Higgins, chief markets economist at Capital Economics, believes it may not signal a long-term trend, given the continued uncertainty surrounding inflation and monetary policy.